If you didn’t hear about Silicon Valley Bank and Signature Bank failing over the weekend, I guess you have been living under a rock. With all of FinTwit looking for comparisons to 2008 we see banks running dry on liquidity, mass withdrawals and the consumer worried about how this is going to cost us in the long run. Let’s be real, the cost is going to trickle down on the people one way or another. Employees were worried their companies bank was failing. How they are going to get a paycheck if your employers funds are not as accessible as they once thought? Scary stuff.

Now considering the lack of trust in the financial system, it’s time to expose the rest of the firms who have caught themselves in a financial bind. Our next guess? Credit Suisse or, as some on Twitter will call, “Credit Sus”.

Credit Suisse is a Swiss multinational investment bank and financial services company headquartered in Zurich, Switzerland. It dates all the way back to 1856. Credit Suisse faced some challenges and controversies over the years, including accusations of tax evasion and involvement in the subprime mortgage crisis of 2008. Today, the bank is known for its underperformance, scandal history, sellers of their assets and now on “Default Watch” following the most recent banking failures.

The firm was delaying publication of its annual report following a last-minute query by US regulators over previous financial statements and stock performance absolutely tanking. Management might be trying to do a little PR to save their own hide but the Street is not buying it.

🚨 BREAKING 🚨 CREDIT SUISSE’S DEFAULT SWAPS HIT NEW ALL TIME HIGH

Insurance to protect against default on their bonds is skyrocketing. #DebitSuisse $CS #CreditSuisse pic.twitter.com/lVJL6lrIuV

— Wall Street Silver (@WallStreetSilv) March 13, 2023

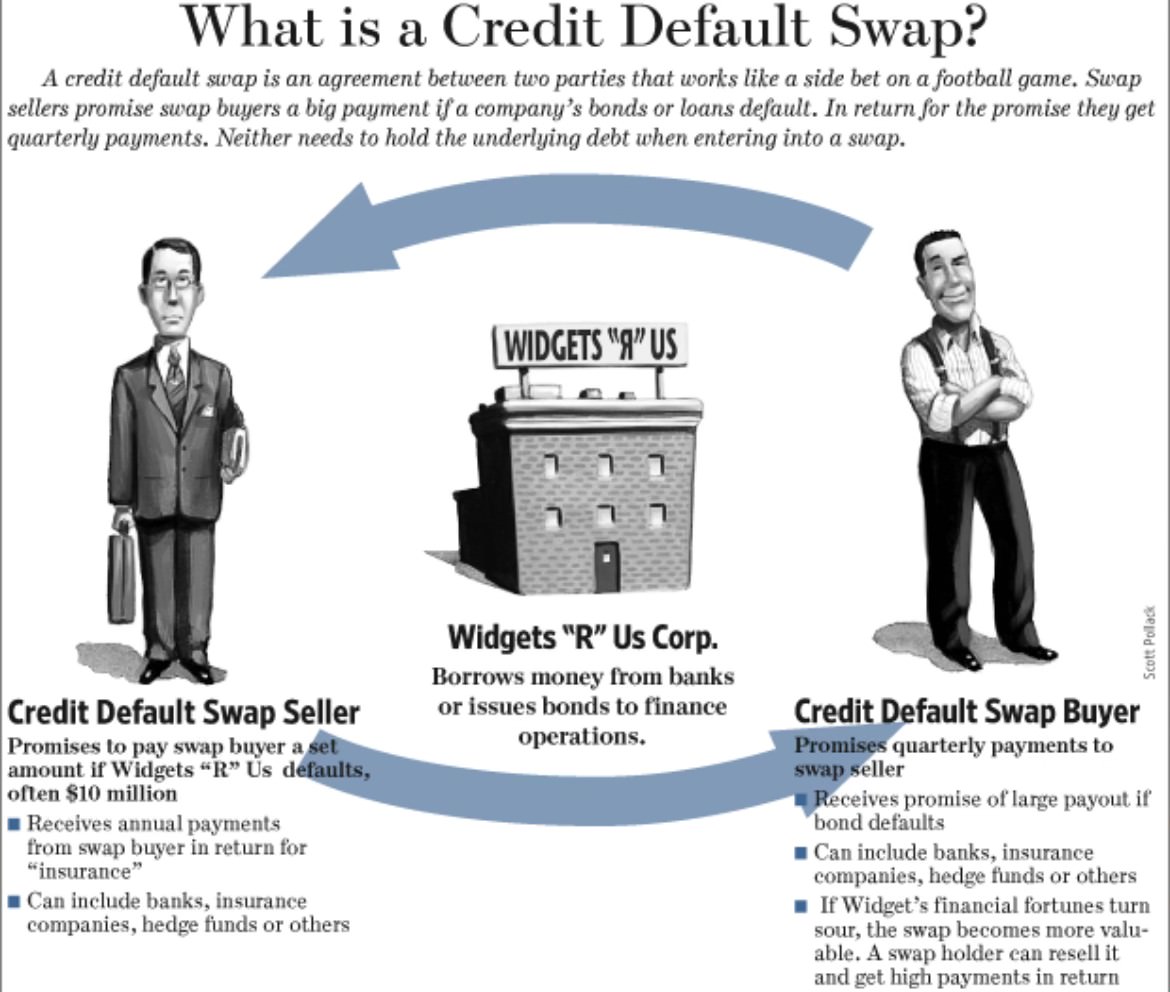

The key indicator this week? THIER CREDIT DEFAULT SWAPS HIT NEW ALL TIME HIGH. In simplistic terms: traders are ultimately looking for insurance to protect against default on their bonds, is skyrocketing.

As the race to get in position is on, premiums are higher when probability of default or not making accrual payments are higher. As demand grows, all it leads to is more of the Street is willing to pay big bucks to protect them selves from CS essentially defaulting.

Credit Default Swaps, a now famous term after Michael Burry, The Big Short guy made his fortune shorting the housing market pre-financial crisis. The man is only going to get richer as he is seeing the writing on the wall again.

Now the respective Federal Reserves across know that banks own long-term paper at extremely low interest rates. Ultimately, they have to decide, are we going to stay the course of maintaining inflation or allow the banks on the bubble to essentially fail? We, the consumer and taxpayer, seem screwed no matter what.

The only ones smiling are BTC holders. The Federal Reserve is in a bind. If they raise rates to keep their goal of taming inflation, banks fail (BTC wins) or they bring out the money printer again, and the dollar is screwed (BTC wins again). Risks for US holders that could hurt them is if our government bans BTC. If the government makes it very hard to get money on and off, people find their way to foreign countries to collect. That hurts the United States anyway.

Most of us have yet to learn our lesson from our previous mistakes, as SVB had a Moody’s credit rating of ‘A’ just three days ago before the news broke that the firm was under water. Same way Mortgage Backed Securities had good ratings before we went to economic hell. With more recession idicators flaring and a banking crisis is on the horizon, investors are now betting on the end of the U.S Banking system as we know it.

Leave A Comment